Efficient and Precise P&L Explain

P&L explain, also known as P&L attribution, helps decipher daily changes in portfolio value by showing which changes came from portfolio activity, time effects, and market risk factors. In MASTIX Derivatives Studio, that explain is built on efficient sensitivity calculations, so the attribution can be produced quickly and with high precision.

P&L explain is not mainly a reporting exercise. It is the test of whether a valuation workflow can show what changed, why it changed, and whether the explanation can be trusted.

When that explanation depends on separate reports, approximations, or manual reconciliation, it usually arrives too late and with too many gaps. A stronger approach is to treat attribution as a direct consequence of the valuation itself.

What a good P&L explain needs to do

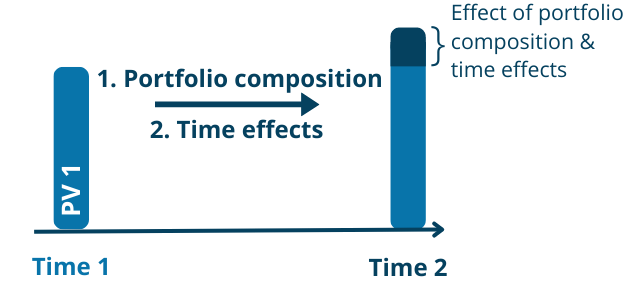

A useful P&L explain should separate the movement in value into a small number of interpretable drivers:

- changes in portfolio composition

- time effects such as cash flows, fixings, and discounting

- changes in market data

That sounds straightforward, but the market-data part is where many workflows break down. If the portfolio is exposed to many risk factors, the explain depends on having a broad and reliable sensitivity set. Without that, the result becomes a rough approximation or a reconciliation exercise between different systems.

Figure 1: Portfolio composition and time effects.

Benchmark sensitivities as the foundation

The cleanest way to explain market-driven P&L is to express it through benchmark instruments and the portfolio sensitivities to those instruments.

That gives you:

- a decomposition in tradeable market terms

- a consistent way to connect risk-factor moves to portfolio value changes

- a foundation that can be reused across explain, scenario analysis, and broader risk workflows

Using first-order sensitivities, the change in portfolio value can be approximated directly from the observed moves in the underlying factors. The problem is not the mathematics. The problem is getting the full benchmark sensitivity set fast enough, and with enough coverage, to make the explanation operationally useful.

Where legacy workflows struggle

In many legacy setups, sensitivities are still estimated through repeated bump-and-revalue calculations:

- shift one input

- rerun the valuation

- measure the difference

- repeat for the next factor

At small scale, that may be acceptable. At portfolio scale, it quickly becomes expensive and slow. More importantly, it breaks the connection between the original valuation and the explanation of the move. The team ends up stitching the answer together after the fact.

That is exactly the failure mode MASTIX Derivatives Studio is designed to avoid.

AAD changes the operating model

MASTIX Derivatives Studio uses Adjoint Algorithmic Differentiation (AAD) to compute sensitivities as part of the valuation itself.

That changes P&L explain in three important ways:

- the full sensitivity set is produced from the same analytical pass as the valuation

- the explanation stays connected to the calculation that produced the result

- attribution becomes fast enough to support investigation, not just documentation

This is the key distinction. AAD is not a reporting add-on. It is part of the engine. That is why the explain can be both precise and operationally useful.

What can be attributed

Once the sensitivity foundation is in place, the explain can be organized into practical components.

Portfolio composition

- closed and matured trades

- new trades

- position changes over the period

Time effects

- cash flows paid

- fixings set

- discounting and passage of time on remaining cash flows

Market data

- benchmark-instrument moves

- benchmark-instrument harmonization when the cash-flow structure changes over time

- curve changes

- other market-factor moves relevant to the portfolio

This gives teams a decomposition that is both technically grounded and usable in real review workflows.

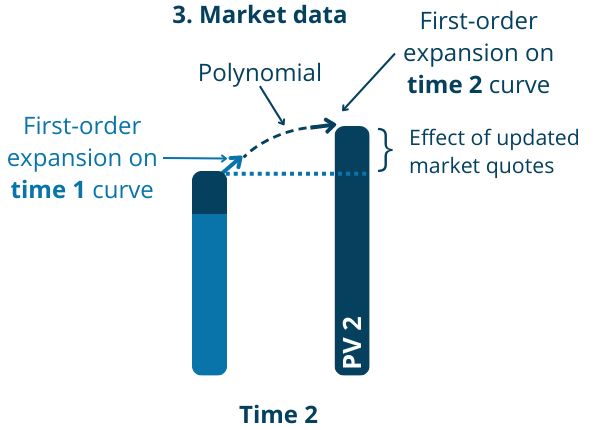

Increasing accuracy with delta interpolation

When sensitivities are available at both time points, the explain can be refined beyond a first-order approximation.

The change in portfolio value can be approximated using a second-degree polynomial in each risk factor. By fitting that polynomial with sensitivities from both time points, the explain can include a second-order attribution term for each risk factor. This delta interpolation captures more of the actual move while staying anchored in the same sensitivity-based framework.

Figure 2: Updated market data and delta interpolation.

The important point is not just mathematical elegance. The refinement still rests on the same underlying engine and the same sensitivity set, rather than introducing a second explanatory workflow.

The same foundation also supports VaR attribution

The same logic extends beyond daily P&L explain.

For Value-at-Risk attribution, the change in value is driven by VaR scenarios rather than observed daily market moves, but the attribution structure is the same:

- identify the relevant factor moves

- apply the sensitivity-based decomposition

- understand which drivers contribute most to the result

VaR attribution helps show how risk factors influence the portfolio under stressed or extreme market conditions. That can be used to identify vulnerabilities and evaluate strategies to improve portfolio resilience.

P&L explain in practice

With MASTIX Derivatives Studio, the explain does not need a separate configuration layer or a separate reconciliation workflow. All sensitivities are obtained through AAD without additional setup.

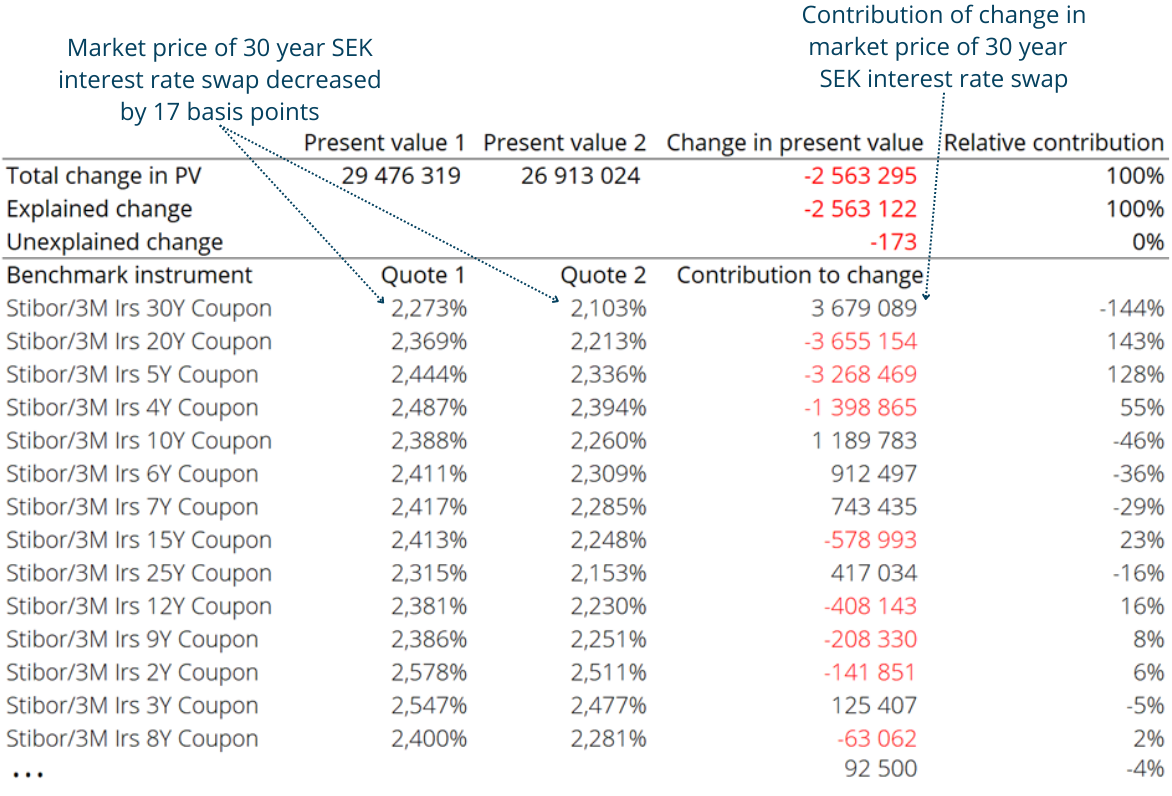

Whenever a calculation is run with two different sets of inputs, attribution can be produced directly from the same engine. The output shows:

- which inputs changed

- how much they changed

- how much each change contributed to the movement in value

That analysis can be accessed through the Excel add-in or through the API, which matters because a good explain is only useful if teams can run it where they already work.

Figure 3: Example attribution output for the present value of a portfolio of interest rate swaps. Only the first benchmark instruments are shown.

Why this matters

The value of a good P&L explain is not that it produces a prettier breakdown. The value is that it changes how quickly a team can move from:

- a surprising result

- to the drivers of that result

- to a decision about what to do next

When sensitivities come from the valuation itself, P&L explain stops being a forensic exercise after the fact. It becomes part of the same analytical workflow as valuation, scenario analysis, and risk review.

That is the real advantage: faster investigation, fewer gaps, and explanations that hold up under scrutiny.